Residential development site sales in Metro Vancouver topped $4.5 Billion in 2016. It’s a staggering value only made possible by the confluence of a variety of local and international market forces including: incoming capital, a feverish residential real estate market, and a perceived lack of quality land available for sale. Each of these factors seemed to create the perfect storm in late 2015 and early to mid-2016 and have played a large part in driving land values to record highs.

To put the year we’ve had into perspective, the total land transaction value for 2016 almost matches the previous two years combined ($2.5B for 2015, $2.4B for 2014).

Here is a brief look at each of the 10 largest land deals of 2016:

#1 – Oakridge Transit Centre, 949 West 41st Avenue, Vancouver

Price: $440 Million

Price: $440 Million

Site Area: 13.8 acres

Vendor: Translink

Purchaser: Intergulf Developments / Modern Green Development

The goods: This was by far the biggest land deal of the year – though the deal is structured to be paid over five years. The former bus barn site was declared surplus land several years ago by Translink and the City of Vancouver initiated a planning policy for the site and surrounding area in 2014. The planning policy was approved in December 2015 to allow for over 1,265,000 SF of density in several low and midrise buildings.

Shortly thereafter the “OTC” site was marketed by Cushman Wakefield. The site secured offers from 14 potential buyers in the spring of 2016 and was ultimately sold to a partnership between Intergulf and Modern Green Development.

A listing video overview can be viewed here: https://youtu.be/GILwlBuOBRQ

#2 – Pearson Dogwood Lands, 650 West 57th Avenue, Vancouver

Price: $299.6 Million

Site Area: 25.4 acres

Vendor: Vancouver Coastal Health

Purchaser: Onni

The goods: This prime site at Cambie and 57th was sold by Vancouver Coastal Health in 2014 as part of a phased deal with Onni. The bulk of the sale formally completed in March. A formal rezoning application has now been submitted which contemplates over 3 Million SF of density, to be completed in five phases with over 10 towers, several mid-rises and a future Canada Line Station. The deal includes replacement of existing VCH facilities on-site.

#3 – Molson Brewery Lands, 1550 Burrard Street & 1655 West 1st Avenue, Vancouver

Price: $185 Million

Site Area: 7.7 acres

Vendor: Molson Coors

Purchaser: Concord Pacific

The goods: Though not the largest deal of the year, this one certainly generated a lot of buzz in the marketplace, and is the only sale on this list that is not a residential land sale – at least based on current zoning policy. The sale closed on March 31 after being listed by Simon Lim of Colliers in 2015. The site is currently zoned M-2 which only allows for manufacturing/industrial uses and is still occupied by Molson on a leaseback basis until their eventual move. Details remain scarce on Concord’s future plans for the site, though it will almost certainly include a substantial commercial component.

#4 – 1444 Alberni Street & 740 Nicola Street

Price: $170.1 Million

Site Area: 43,300 SF

Vendor: Wall Financial

Purchaser: Landa Global/Asia Standard

The goods: This full city-block located in the West End of Downtown Vancouver was redesignated as part of the West End Community Plan, adopted in early 2014. The site is currently improved with an office and apartment tower built in the 1970’s. Wall had acquired the site in March 2014 for $83.5 Million and subsequently sold through Simon Lim of Colliers after a bid process in late 2015. The sale closed in April 2016. It is expected that the property will be completely redeveloped with two 40+ storey condo towers.

#5 – Brighouse Square, 6340-6390 No. 3 Road, Richmond

Price: $73,500,000

Site Area: 3.6 acres

Vendor: Sanna Enterprises

Purchaser: YYH Development Ltd.

The goods: Brighouse Square is a retail strip plaza at No. 3 Road and Cook Road across from Richmond Centre. The site sold as a potential future residential development play in May 2016 to a Chinese development group. It had been designated as ‘Urban Core T6’ in Richmond’s City Centre Plan to allow for mixed residential and retail. Simon Lim of Colliers acted as the broker in the off-market deal.

#6 – 1745 West 8th Avenue, Vancouver

Price: $70,000,000

Site Area: 56,550 SF

Vendor: CIBC

Purchaser: Delta Land

The goods: Our team marketed and sold this C-3A zoned, Fairview office building/development site on behalf of CIBC in late 2015, with the sale closing in February 2016. The site achieved 9 offers, with the successful buyer being Delta Land Development. CIBC is leasing the property back until mid-2017 after which time Delta will likely release plans for the property.

#7 – 1059-1075 Nelson Street, Vancouver

Price: $68,000,000

Site Area: 17,292 SF

Vendor: Suncom

Purchaser: Shan Gao

The goods: In one of the more interesting sales in recent Vancouver history, this assembly of two non-descript walkup apartment buildings sold three times in just under two years in a series of events documented by Ian Young. Our team acted for Wall Financial in the original assembly and subsequent sale in January 2016. The site flipped in February 2016 for $68,000,000 to a Chinese buyer who remains generally unknown to the market.

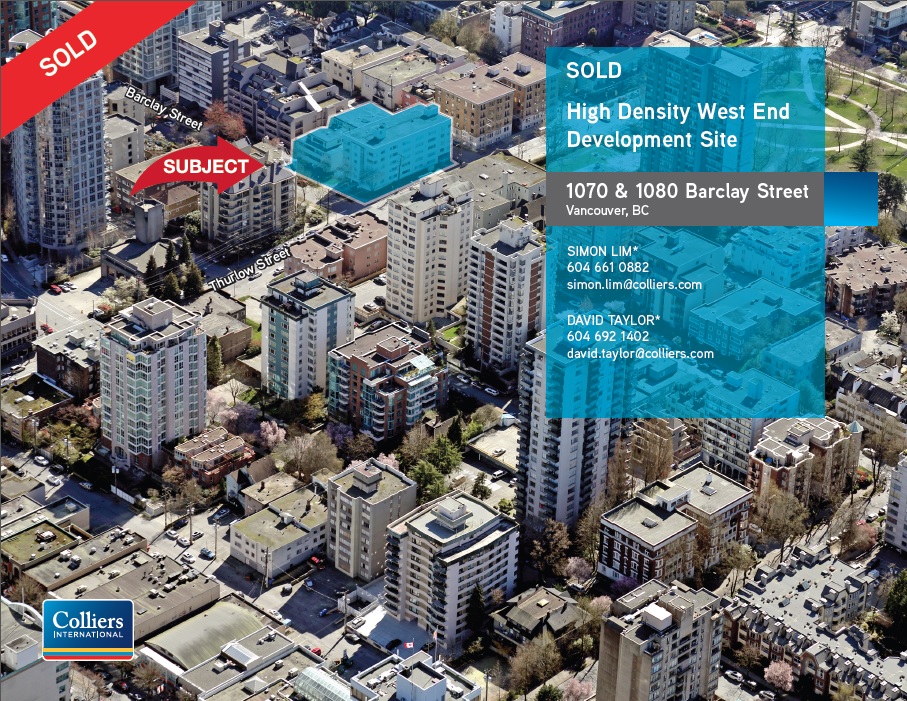

#8 – 1070-1080 Barclay Street, Vancouver

#8 – 1070-1080 Barclay Street, Vancouver

Price: $59,000,000

Site Area: 17,292 SF

Vendor: Two Private Local Investors

Purchaser: Bosa Properties

The goods: Just across the lane from #7 on this list, this assembly of two apartment buildings was listed by our team in late 2015 and sold after multiple offers to Bosa Properties. The site was also re-designated in the West End Community Plan to allow for towers up to 550 ft. (subject to shadowing). Bosa also secured the neighbouring strata building at 1060 Barclay. The deal closed in February 2016.

#9 – 1818-1862 West Broadway, Vancouver

#9 – 1818-1862 West Broadway, Vancouver

Price: $56,250,000

Site Area: 37,500 SF

Vendor: Private Local Investors

Purchaser: Suncom

The goods: This assembly of lots on West Broadway near Burrard Street was sold by our team in September 2016. The assembled site comprises 300 feet of frontage and the existing C-3A zoning allows for up to 3.0 FSR residential with retail.

#10 – 1810 Alberni Street & 703-751 Denman Street

#10 – 1810 Alberni Street & 703-751 Denman Street

Price: $55,000,000

Site Area: 17,292 SF

Vendor: Local Investor

Purchaser: Landa Global

The goods: This West End development site was sold by the Simon Lim team in September 2016 after a listing process. The Property is currently zoned C-5A (West End Commercial), which provides for 2.20 FSR with potential to increase density to 7.00 FSR, and by heritage density increasing up to 7.70 FSR. It is situated in Lower Robson Area A of the West End Community Plan – designation consistent with the amended C-5A Zoning (no rezoning required).

Honourable Mentions:

Below are a couple of notable transactions that formally closed in 2016, but we are not including as they aren’t technically relevant sale deals for the purposes of this analysis.

- 508 Helmcken Street – this site, more commonly known by its project name “8X on the Park“, is part of a land exhange that was negotiated back in late 2012 with the City of Vancouver. The completion of the Jubilee House social housing replacement project triggered the land exchange so that Brenhill Development can move forward with the construction. The sale value was $83,500,000.

1166 West Pender Street – our team acted in this $71,400,000 sale, closing in April 2016. The site is currently improved with a 15-storey office building that the Purchaser, Reliance Properties, intends on redeveloping, though we have not considered it a pure land play as with the transactions above.

1166 West Pender Street – our team acted in this $71,400,000 sale, closing in April 2016. The site is currently improved with a 15-storey office building that the Purchaser, Reliance Properties, intends on redeveloping, though we have not considered it a pure land play as with the transactions above.

Some notes from the above list:

- 9 of the 10 largest land deals in Metro Vancouver took place in the City of Vancouver

- 8 of 10 were sold by market bid process (the other 2 were ‘off-market’)

- 3 of 10 were bought by well-established ‘local’ development groups, the other buyers were offshore or ‘new-entrant’ development companies

- 8 of 10 will require a rezoning process before development can occur