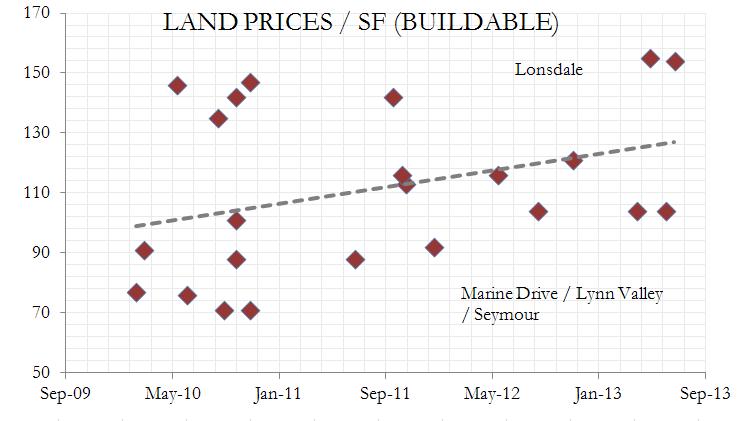

North Vancouver Development Site Transactions 2010-2013

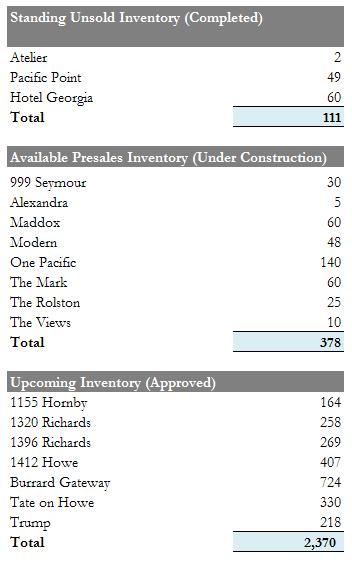

Here’s a snapshot of currently selling downtown condo projects in terms of inventory. Also included are projects likely to be released in the next 12 months. Overall, available inventory seems to be in healthy and balanced territory, though some larger upcoming projects scheduled to be offered in the next two years may have an impact on the market with well over 2,000 units.

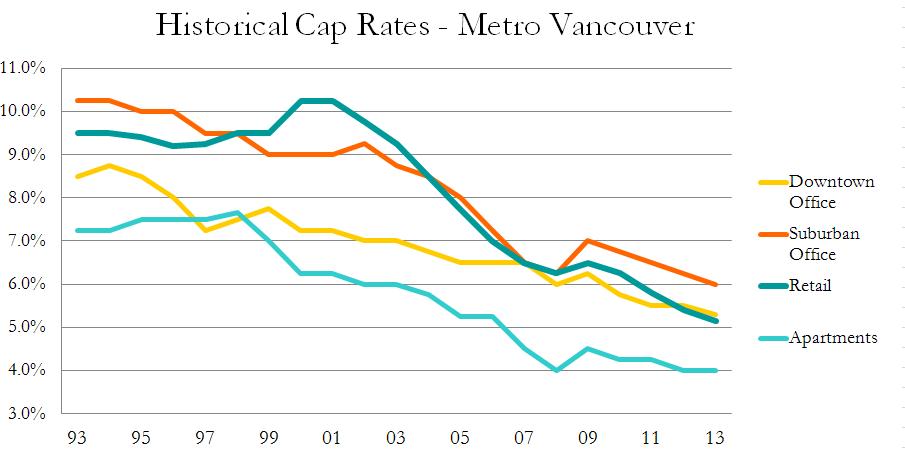

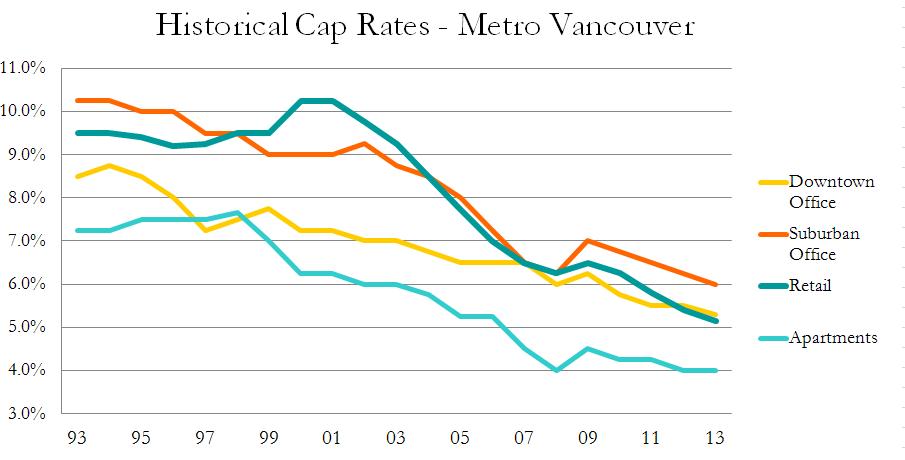

As we’re now well into Q4 2013, a brief look at average cap rates in Metro Vancouver shows (surprise!) no significant change from 2012. Underpinned by an environment of continually cheap debt, cap rates have been flat or remain in slight decline, and now 100 BPS below the rolling 10 year average of 6.2%.

Average Cap Rates 1993-2013

Of course, only in rare cases are Vancouver buyers truly finding yield; it is often more of a ‘safety’ play. With a healthy supply of potential (and anxious) private equity buyers that have amassed significant, undeployed cash reserves in reaction to depressed and uncertain market conditions in recent years, cap rates are being bid down now as much as ever. This, coupled with fiscal authorities in both Canada and the United States continuing to maintain interest rates at historically low levels have resulted in the continuation of historically low cap rates in Vancouver.

The first signs of a shift in this trend may already be occurring with a slight downward trend in transaction activity so far in 2013. A continuation of this trend in 2014 combined with a changing economic/interest rate environment and potentially volatile leasing markets (particularly in office) may finally exert upward pressure on cap rates.

…just don’t tell owners…

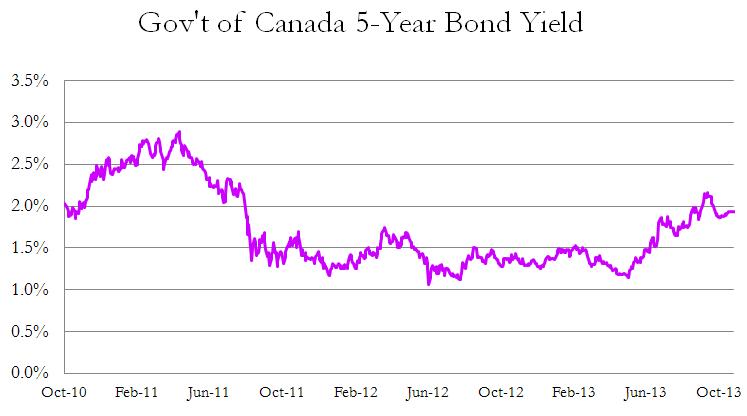

5-Year Bond Yield, October 2013

12-unit Gleneagles townhouse project proposed in West Vancouver

A new proposal has surfaced for the parking lot next to Waterfront Station.

The redesigned project includes a 26-storey, 416,000 SF office tower, shaped like a tree, cantilevered over the existing station building.

Architect: James Cheng

Details: https://bit.ly/46aUB0W