The target DCL and CAC rates are adjusted annually to keep pace with changes in property values and construction costs.

The proposed adjustment for 2022 is a increase of 1.2%. The increase returns to an inflationary trend after the pandemic forced a decrease of 0.8% for 2021.

Here are the new proposed rates:

The new target rates will become effective September 2021.

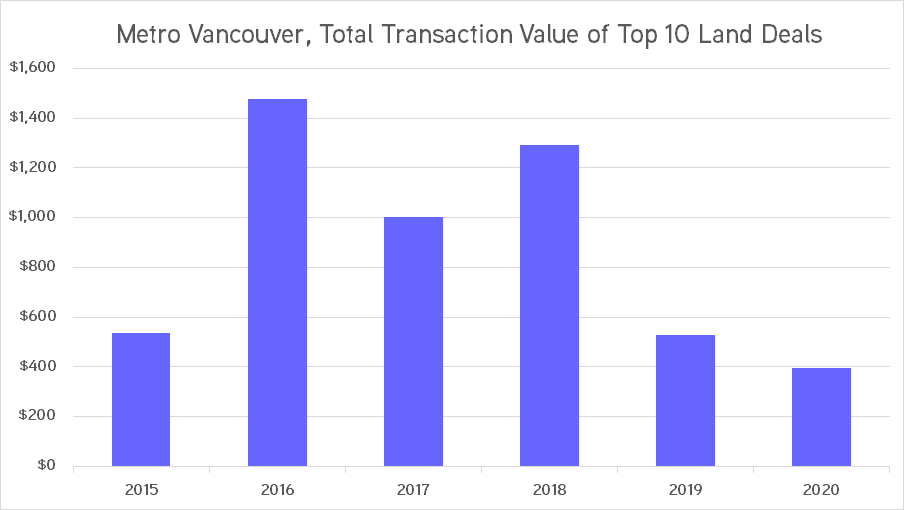

In past years, compiling a list of the Top 10 land sales in Metro Vancouver was a daunting task; not only was there such a large volume of sales transactions to sift through, but the size of the larger deals was staggering, with the total of just these 10 deals alone eclipsing $1 Billion annually for the period of 2016-2018.

It was an overheated market that was due for a correction, and this decline began in mid-2018.

The more recent global pandemic that emerged in March 2020 has and will continue to have major implications for almost every facet of local and global real estate. For the overall Metro Vancouver land market however, the pandemic can somewhat be characterized as “beating a dead horse”. 2019 sales volume was already down by more than half the previous year.

A pullback from developers to acquire more land amid a significant condo development pipeline in most submarkets was a primary reason. Land for both rental residential and commercial development has remained relatively scarce which has offset some of the decline in condo land activity. Likewise, more recent activity suggests a return of demand for condo land in the suburbs, though core luxury condo sites have essentially fallen off the radar. Land for industrial development is now acutely scarce, with each transaction seeming to support a record value per acre.

While the 2016-2018 market may seem like a distant memory now, there are reasons for optimism heading into 2021. One sentiment emerging from this trying year is that both private and instituational investors continue to be bullish on the long-term prospects for Vancouver and a projected demand for continued residential, commercial and industrial development. Any return to inflows of international capital, either for individual strata units, or for land deals, will also contribute to momentum in the years ahead.

Here’s a look at each of the 10 largest land deals of 2020:

The goods: The largest land deal of 2020 would not have even cracked the Top 10 list in recent years, which speaks to the shift in the market. The sale of this site on Elmbridge Way in the Oval Village area of Richmond’s City Centre area has an existing rezoning application for three residential towers, plus commercial and hotel space. The deal was negotiated in 2019 and continues Landa Global’s expansion in the overall Vancouver marketplace.

The goods: Another industrial land sale nears the top of the list; this one in Langley on an underutilized site zoned for Heavy Industrial uses. No word yet on plans for redevelopment of the site.

The goods: This sale involved a former Esso gas station site at the Northeast corner of Cambie and West 41st Avenue. Coromandel had acquired the site in October 2014 for $15,800,000. In 2018, an update to the Cambie Corridor Plan redesignated the site to allow for a potential mixed-use tower. No rezoning applications have yet been filed.

The goods: Mosaic Homes purchased this townhouse development site on Burke Mountain from the City of Coquitlam. The preliminary plan for the site calls for 167 townhouse units.

The goods: Just a few short years ago, Metrotown tower sites were selling monthly at record valuations. Today, the market for sites has cooled considerably amid a perceived oversupply of future condo product. This sale on Wilson represents an assembly, as Bosa controls the two neighboring sites at 5977 and 5979 Wilson. The price per SF for the site is considerably lower than what could have been achieved at the peak of the market, and was likely a motivating factor in this deal having been completed in 2020.

The goods: This site on the West side of Cambie at West 7th Avenue, mostly known as the Robinson Lighting property is a fully tenanted retail property that has future development potential under it’s C-3A zoning.

8. 140-150 West 4th Avenue & 2004 Columbia Street, Vancouver

The goods: This sale involved an I-1 zoned site in the burgeoning Mount Pleasant Light industrial/office district. A development application for the site envisions a 4-storey commercial building at a total density of 3.0 FSR.

9. 475 West Hastings Street, Vancouver

Price: $31 Million

Site Area: 9,360 SF

Vendor: Private Investor

Purchaser: Private Investor

The goods: This site at the Northeast corner of West Hastings and Richards Street in Downtown Vancouver has long been home to tenants including Mr. Big and Tall. While no redevelopment plans have been made public, the intent appears to be a midrise hotel development.

The goods: This property is a retail strip mall in Surrey’s City Centre. Tien Sher has a rezoning application to allow for a high density mixed use development including 500 residential units and commercial space.

Some notes from the above list:

5 of the 10 largest land deals in Metro Vancouver took place in the City of Vancouver (up from just 1 last year)

3 of 10 were sold by market bid process (the other 7 were ‘off-market’)

All 10 were bought by well-established ‘local’ development groups, with previously active offshore buyers absent from these large deals.

Have a question or a comment on any of the transactions above? Please feel free to contact me.

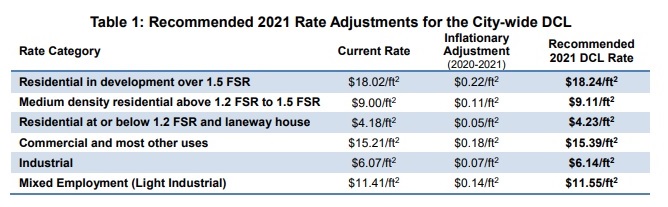

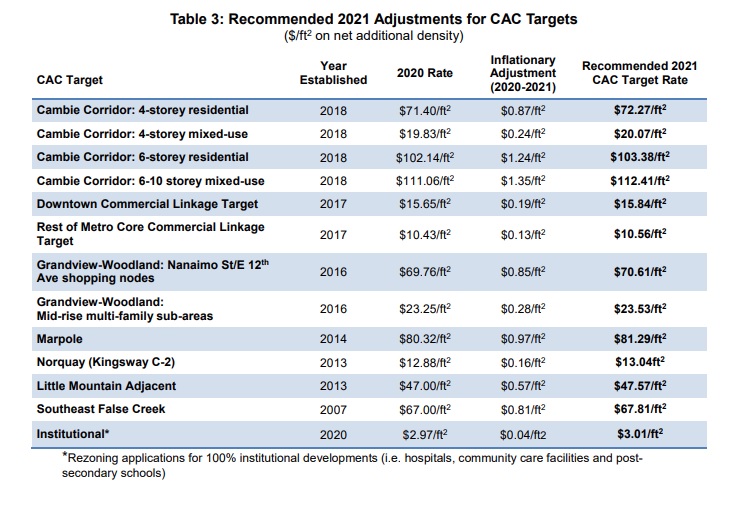

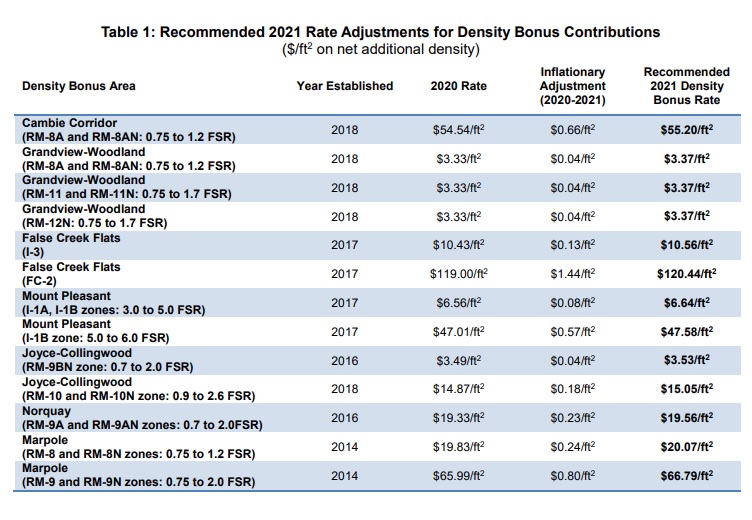

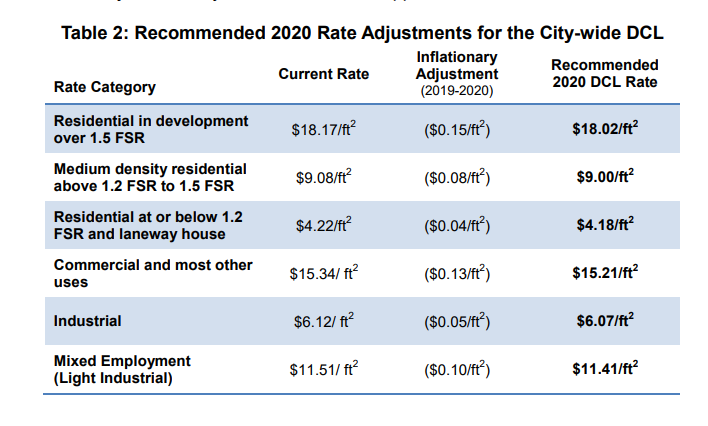

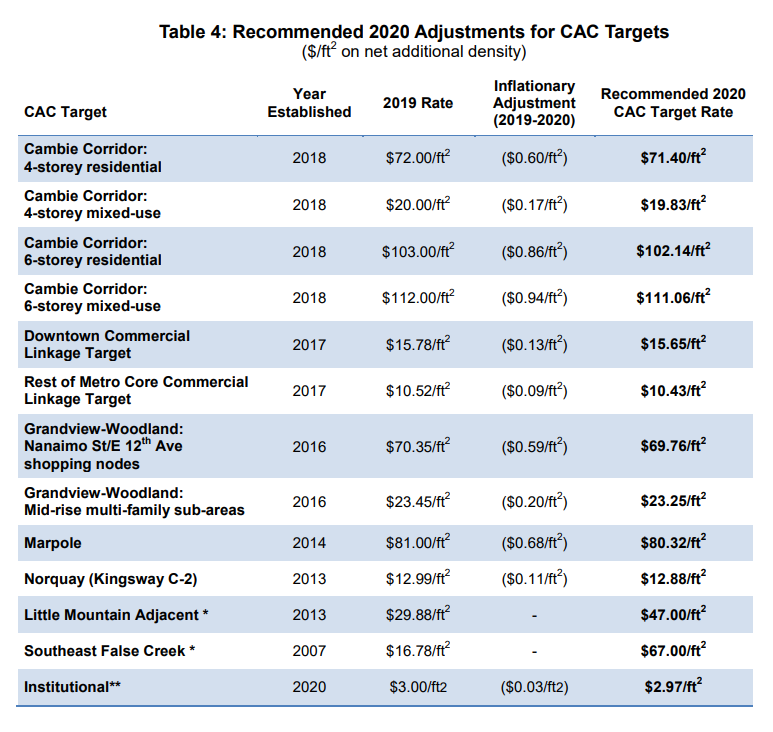

The target DCL and CAC rates are adjusted annually to keep pace with changes in property values and construction costs.

The proposed adjustment for 2021 is a decrease of 0.8%; the first decrease since the annual inflationary index was developed by the City in 2011.

Here are the new proposed rates:

The new target rates will become effective September 2020.

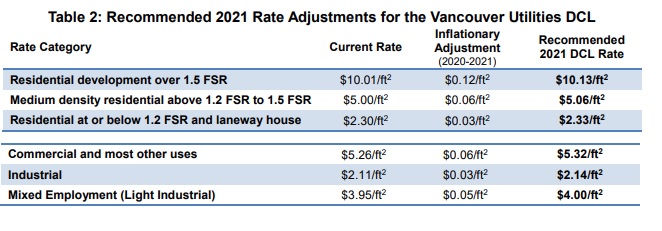

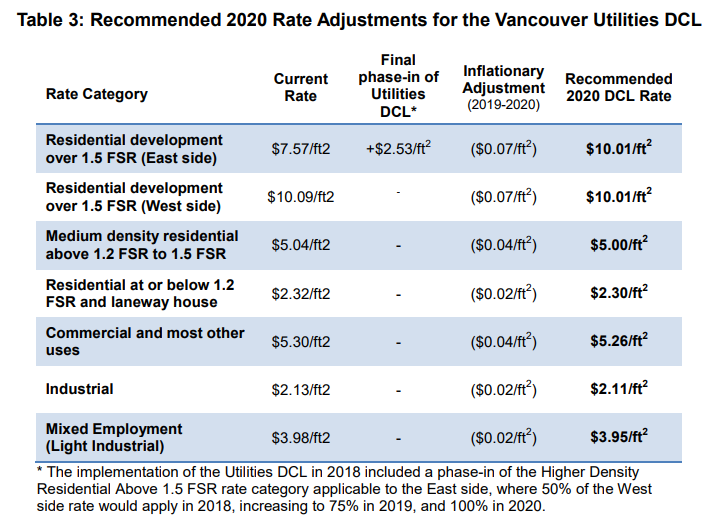

The report also recommends proceeding with the final phase-in of the Vancouver Utilities DCL rate for high-density residential development on the east side that was approved by Council in July 2018, and the adjustments of the Little Mountain and Southeast False Creek CAC Targets that were approved by Council with the updated CAC Policy in January 2020.

The new target rates for these areas are as follows:

Little Mountain Adjacent: The Little Mountain Adjacent CAC Target will be increased from its current level of $29.88 per sq.ft. to $47.00 per sq.ft. Southeast False Creek: The CAC Target in Southeast False Creek (SEFC) will be increased from its current level of $16.78 per sq.ft. to $67.00 per sq.ft.

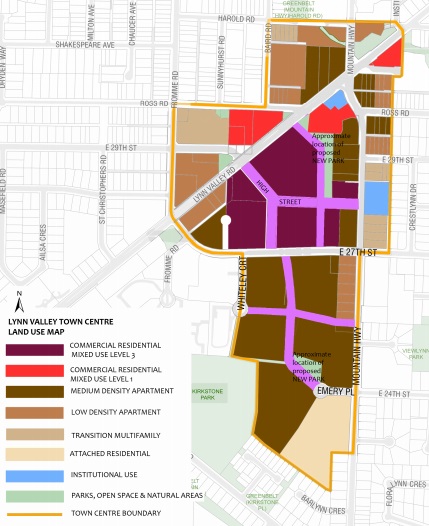

Lynn Valley is one of North Vancouver’s two Town Centre areas. It’s also the District of North Vancouver’s Municipal Town Centre in the Metro context, which is defined as “a municipal-wide centre or hub with medium and higher density uses including residential, commercial, employment, recreational and civic”.

Located in the heart of Lynn Valley, the Town Centre core is currently focused around Lynn Valley Centre, and the new Lynn Valley library and civic plaza. From the District’s OCP: “Heritage buildings and features, parks and views to local mountains reflect the rich cultural and natural history of Lynn Valley. Building on the quality design, liveliness and sense of place initiated by the new Lynn Valley library and civic plaza, there is an opportunity to revitalize the Town Centre into a more vibrant, pedestrian oriented, mixed use centre with housing choices and inviting street level shopping along a High Street with sidewalk cafes and community spaces. Redevelopment of the Town Centre also provides an opportunity to increase the diversity of housing choices in an area close to services, shops, jobs and transit.”

There has been solid growth of residential development over the past several years, though future inventory remains low given the lack of land for development coupled with the District of North Vancouver’s more recent efforts to slow new development.

The Policy Background

The District of North Vancouver created a new Official Community Plan (“OCP”) in 2011, and the land use objective for Lynn Valley Town Centre was to “accommodate approximately 2,500 new units” over a twenty year time horizon.

The OCP was further refined for Lynn Valley in 2013/2014 and opened up a number of development opportunities, but confined these opportunities to primarily the relatively small area between Mountain Highway and Lynn Valley Road.

Lynn Valley Centre Land Use Map

A number of development projects have been initiated or completed (this is expanded upon below).

The rezoning designations contemplate mostly low to medium density woodframe residential except on key sites including the Lynn Valley Centre Mall site, which were given higher density designations. There are only a handful of properties with a commercial only designation.

Here is a video outlining the overall urban design/public realm concept:

Lynn Valley Centre mall was determined to be a focal point of the plan area. The 12-acre shopping centre was acquired by Bosa Development in 2003 for $36,000,000, or an 8.6% cap rate and subsequently rezoned in 2014 (further details below). The adjacent 2.8 acre Safeway site is separately owned by Crombie REIT.

As with the other growth centres in the District of North Vancouver, the appearance of rapid growth and attendant impacts such as traffic and construction has led to increasing opposition for new rezoning applications. The District of North Vancouver is now undertaking a lengthy review of their OCP to determine what adjustments need to be made to keep growth under control and to deliver on promises of affordability.

The Residential Market

Traditionally Lynn Valley has been a single family and ground-oriented community/submarket. Some older lowrise condo buildings exist on side streets near the mall site. The vast majority of condo product in Lynn Valley has been built in the Town Centre area in the last 15 years, mostly as a result of the new OCP in 2011.

The lack of condo buildings in Lynn Valley has generally supported increased pricing, particularly given price points relative to single family, which can reach well in excess of $2 Million for new product.

Here is a snapshot of the currently active condo listings on MLS:

# of Active Condo Listings

10

Median Sale Price

$620,000

Median Age (years)

10

Median $/SF (All)

$766

Median $/SF (2yrs old or newer)

$881

Older woodframe condos typically trade in the $500-600 per SF range, with newer concrete condos in the $850-950 per SF range.

Recently completed projects include:

Polygon’s 68-unit Juniper at 2517 Mountain Highway. It is woodframe construction. Completed in 2019. Recent resales show values of $825-850 per SF. Taluswood has been another successful subsequent phase nearing completion across Library Lane.

Bosa’s first phase of the Residences at Lynn Valley included a 108-unit, 7-storey concrete building on the Eastern portion of the Mall site. It was completed in 2018. Resales values range from $750-1,000 per SF.

Canyon Springs is another Polygon project just down the street, completed in 2015. 108-units and also woodframe, recent resales show a range of $750-850 per SF.

Overall, about 800 units have been built in Lynn Valley since the OCP was adopted, and most of these have now been sold.

New Construction & Proposed Units

Phases 2 and 3 of Residences at Lynn Valley are nearing completion. These terraced buildings up to 12-storeys in height total an additional 250 units.

Approximately 400 units are in the proposal stage for Lynn Valley, the largest of which is Mosaic Homes’ Emery Village project, just South of Lynn Valley Centre, which contemplates 327 condo units and 84 rental units in a phased development. The District approved rezoning in 2018 and development permit for the first phases in 2019.

Rental

The District of North Vancouver has a total inventory of only approximately 1,200 units of purpose built rental units, and less than a quarter of these are located in Lynn Valley (excluding Seniors’ residences which number several hundred more).

Polygon Homes recently completed Hawthorne at Timber Court, a 75-unit woodframe rental apartment building located adjacent their Juniper project. The Hawthorne building is taking registrations for lease, and has also recently been listed for sale.

The Land Market

After completion of the OCP and amid a rising residential real estate market, a number of larger development sites have transacted over the past five years as the market has continually justfied redevelopment of older lowrise apartment properties on relatively underutilized sites. Some of these include:

Mountain Court, this 4.1 acre site housed 72 older rental units and was acquired by Polygon in 2015 for what would eventually become Timber Court (Juniper, Hawthorne & Talisman). The $25,640,000 price tag equated to approximately $80 per buildable SF.

Mosaic Homes acquired the aforementioned 5.1 acre Emery Village site in 2016 for $39,550,000 or $75 per buildable SF.

There is currently approximately 300,000 SF of commercial space in the Lynn Valley Town Centre area, over half of which (170,000 SF) is in the Lynn Valley Centre mall. There have not been any significant recent investment transactions in the area.

In early 2019, the City of Burnaby introduced a new Rental Use Zoning Policy intended to support construction of new rental units and to prevent the loss of rental units to demolition for condos.

Since then, the City has monitoring rezoning applications and receiving feedback from applicants and stakeholders regarding the policy. The biggest feedback has been from developers regarding the City’s proposed “vacancy control” whereby rent increases were limited between tenancies.

As a result, the City of Burnaby is recommending a number of amendments to the Rental Use Zoning Policy, to be approved at the Planning and Developement Committee next week.

These changes include:

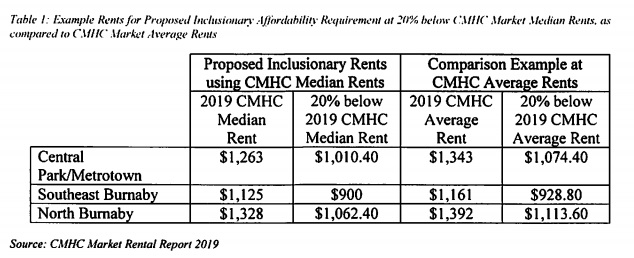

1. Use of CMHC Market Median Rents instead of CMHC Market Average Rents

The Rental Use Zoning Policy currently uses CMHC market average rents as the metric from which below-market rents are calculated. However, the use of market average rents may result in significant fluctuations over time, as unusually high or low rents skew the average amount. To ensure a more accurate reflection of current market rents, staff propose using CMHC market median rents.

2. Amend Inclusionary Requirement to Deliver Greater Affordability

The Rental Use Zoning Policy currently requires all new developments in Community Plan areas to provide 20% of the total number of units as rental housing.

The inclusionary units are provided through density provisions under the Multiple Family Residential Rental (RMr) zoning districts. Inclusionary units are currently not subject to affordability criteria and may be rented at market rents. To incentivize affordability, additional market density, known as a density offset, is granted to projects that provide the required rental units at 20% below CMHC market average rents.

The City is now proposing to amend the policy to require the 20% inclusionary requirement to be offered at 20% below CMHC market median rents. As noted, to support the economic viability of these projects, a density offset is available to achieve this new affordability requirement. In addition, staff further recommend that the 20% inclusionary requirement be calculated from the total number of market (strata or rental) units derived from RM and RMs density provisions, as opposed to the total number of all units. This is to ensure that projects that seek to provide additional rental housing, particularly at below-market or non-market rents, are not dis-incentivized to do so due to the methodology for calculating inclusionary units. Overall, both RMr zoning district density and offset densities are not subject to the inclusionary requirement. For reference, the table below illustrates the current starting rents for the proposed below-market inclusionary units at 20% below CMHC market median rents, based on the most recent 2019 CMHC Market Rental Report. CMHC market average rents, as well as 20% below that metric, is also provided in the table below for comparison.

3. Amend RMr Density Provisions, Including Removal of Vacancy Control

The current Rental Use Zoning Policy requires units created by the new RMr density to be subject to vacancy control. The only units not subject to vacancy control are below-market rental units that receive a density offset and rental units permitted in Commercial zones.

The concept of vacancy control has resulted in concerns that few applicants would take advantage of the voluntary RMr density, impacting the delivery of new market rental units in the City. “The development industry has noted the hardship that vacancy control could impose on the long term viability of rental developments as the amount of rent that could be charged on vacant units between tenants would be limited. In particular, the change to the calculation of the RTA maximum allowable rent increase in September 2018 from rate of inflation plus 2%, to rate of inflation only, has increased concerns from landlords regarding the ability to maintain rental properties over time. Finally, and perhaps most importantly, the impact of vacancy control on the ability of the development community, including pension funds, to secure development financing, thus leading to a low uptake of the available density, remains a concern.

To incentivize the use of RMr density provisions, staff support the PDC motion to remove vacancy control. Instead, the affordability of rental units would come from the proposed amendment to require inclusionary units to be offered at 20% below CMHC market median rents. In addition, staff further propose that the use of RMr density above the required inclusionary component be set at a 1:1 ratio of market and CMHC market median rental units. In this case, for every one market rental unit proposed by the applicant, an equivalent one unit at CMHC market median rents would be required. This would assist in meeting the City’s long term affordability objectives in the absence of vacancy control, and create additional below-market rental opportunities for moderate income households. As the discount from market rents would be minimal at CMHC market median rents, a further density offset is not recommended for this new 1; 1 market and CMHC market median rental unit requirement for additional RMr density. “

4. Clarify Use of Density Provisions in Commercial Districts

The Rental Use Zoning Policy also allows developers to offer voluntary rental density in commercial districts, with 49% of the designated commercial floor area within applicable commercial zoning districts to be residential rental housing, provided the remaining 51% of the floor area are typical commercial uses.

The current policy language on the use of density to achieve voluntary rental housing in commercial districts is unclear and warrants clarification. As such, staff propose amending the Rental Use Zoning Policy to specify that rental uses and density from commercial zoning districts may only be achieved after the inclusionary requirement and all multiple family residential densities, including bonus, are fully utilized.

5. Clarify Rental Replacement Requirements

The Rental Use Zoning Policy requires all rental units lost through redevelopment to be replaced in Community Plan areas. This was one of the main original driving factors behind the policy, and will remain in place.

The policy sets the replacement ratio at 1:1 or 20% of the total number of strata units, whichever is greater.

A number of minor clarifications are proposed:

“First, staff propose clarifying that replacement units must be offered at the tenant’s rent level at the time of move out, plus any adjustments based on permitted RTA rent increases during the time between move out and occupancy, to remove vagueness in the current language.

In addition, the replacement ratio would be amended to be 1:1 or 20% of the total number of market (strata or rental) units derived from RM and RMs density provisions, whichever is greater.

Staff further propose amending the rental replacement requirement to apply to redevelopments involving the loss of purpose-built rental buildings with five or more units, as opposed to six or more units, to align with the City’s approved-in-principle Tenant Assistance Policy.

“A more critical amendment is clarifying a potential inconsistency noted by the development industry and BC Housing regarding the City’s desire to prioritize both returning tenants and secure deeper affordability through senior government funding. Under the current policy, applicants are required to provide tenants who are eligible for assistance the opportunity to move into the new replacement units upon completion, by way of a tenant’s right of first refusal. The policy also encourages applicants to pursue senior government funding to achieve greater affordability, including for the replacement units. As senior government funding often requires income testing of tenants to ensure the affordable units are provided to those who need it most, some returning tenants may not qualify, depending on their income. To balance the City’s objectives of prioritizing displaced tenants and housing affordability, staff propose amending the Rental Use Zoning Policy to state that if senior government funding is secured, the non-profit housing operator would prioritize returning tenants for these units, provided they meet funding and eligibility criteria. If any returning tenants do not qualify for the senior government funded units, the applicant would be responsible for accommodating these tenants in other units in the development at their established “move-out” rent (plus RTA increases). Units may include inclusionary units, if available, or any below-market or market rental or strata units in the development, with the units reverting back to its original tenure and affordability requirement, if any, once the returning tenant vacates the unit. Staff also recommends adding a statement in the policy that a tenant’s right of first refusal is contingent on the tenant remaining in good standing as per the RTA. Should a tenant be evicted for cause during the interim period between move out and occupancy, the applicant would not have to offer a replacement unit to this tenant.”