While the City of Vancouver is most often the focus of debate and discussion surrounding the current housing affordability crisis, development pressures are now forcing other municipalities to engage in research and analysis on the issue. Recent public backlash related to the redevelopment of older low-rise apartment buildings has forced staff and council in many Metro Vancouver cities to spend time reviewing the issues.

The Councils of both City of Burnaby and the District of North Vancouver (“DNV”) received reports in the past week from their respective planning departments on issues surrounding housing affordability. In both cases, the reports were prepared primarily for information purposes only and will not immediately result in policy changes; however, the increasing dialogue at the municipal level is sure to have an impact on planning and rezoning policies in these and other municipalities in the near future. Both Burnaby and DNV are grappling with the impending redevelopment under new OCPs that have targeted older apartment buildings in “town centre” areas, though they appear to have differing perspectives on what can actually be done at the municipal level.

Suburban municipalities are well behind the City of Vancouver which was forced to take more severe measures to protect rental housing stock after development pressure in the 80’s and 90’s. Likewise the City of Van has been more progressive on devising and implementing rental incentive policies, to varying degrees of success.

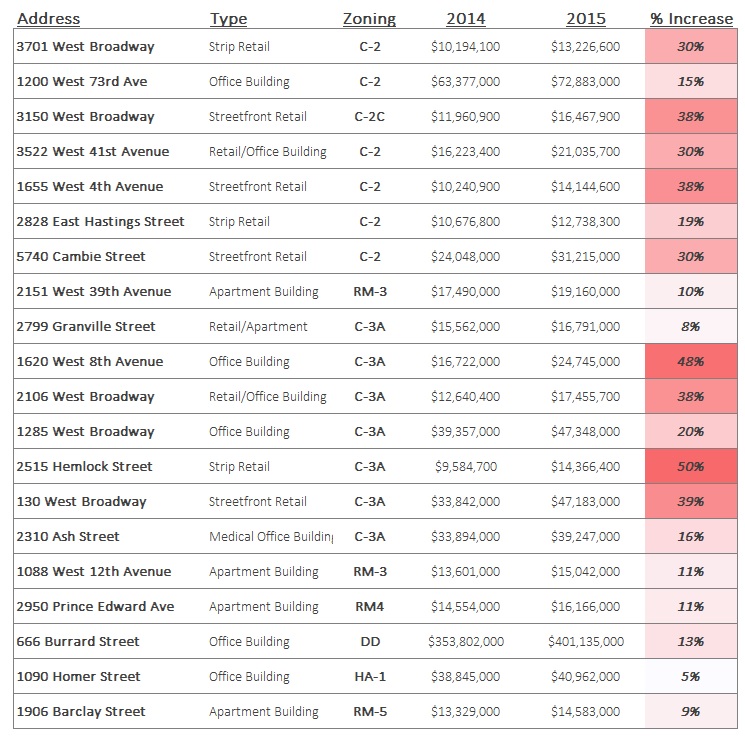

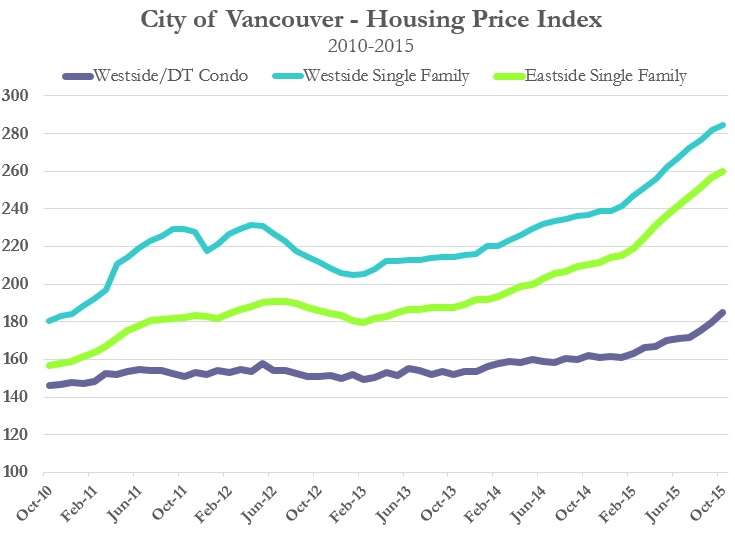

As both single family and condo values increase throughout Metro Vancouver, redevelopment pressures are now mounting in many areas and citizens throughout Metro Vancouver are urging governments to take a harder look at housing affordability. Even sleepy Maple Ridge is feeling pressure on the rental market.

Below is a brief summary of the two reports that went to each City Council with specific focus on the issues identified in each municipality and potential policy implications (or lack thereof):

City of Burnaby – Growth Management and Housing Policies in Burnaby (Nov 4, 2015)

Purpose of Report

“to place the City’s approach to the management of growth within the context of housing policy and demand, tenure and affordability. This report outlines the City’s policy framework for managing growth; reviews the roles and responsibilities of local and senior levels of government in the provision of housing and housing affordability; highlights the City’s legislative role and ability to improve the range of market and non-market housing opportunities and affordability levels; and discusses the constraints faced by local governments to directly provide or influence the supply and/or affordability of housing.

This report has been prepared in response to observations and concerns received by the City regarding new developments within the Town Centre…where existing rental housing sites nearing the end of their building life-cycle have been advanced for redevelopment”.

Here is a recent news clip about a project on Silver Avenue:

Snapshot of Burnaby’s Rental Housing Market

- One third of Burnaby’s dwelling units are rental (32,000 of 96,000)

- 2nd largest rental market (after City of Van – 55,800 units)

- Current apartment vacancy rate of under 1%

- Most town centre areas have buildings from 50s/60s – nearing end of life

- Land costs largely preventing new rental construction despite demand

Role of Municipality and Burnaby Policies to Date

- Rental Conversion Control Policy (1972) -can’t convert rental to strata

- Density Bonus Policy (1997) – allows rezoning, 20% of CAC to non-market

- Tenant Assistance Policy (2015) – requires tenant assistance exceeding RTA

Overall, the City indicates that 7,900 Non-market units have been developed in 154 developments.

Constraints to Addressing Affordable Rental Housing

- City cannot impose a moratorium on demolition of existing apartments

- A “Standard of Maintenance Bylaw” imposed on existing apartment owners would not have the desired effect of increasing supply or addressing affordable rents

- City is looking at ways to build rental housing directly, but needs support of other levels of gov’t

- A requirement for rental replacement would impair feasibility of new projects

The report points out that it is estimated that 25% of all new strata are rented out, equating to 8,400 rental units in new supply.

CONCLUSION

The general conclusion of the report is that any policy in the near-term that would slow the redevelopment in town centre areas would have an overall worse impact on housing affordability by suppressing the supply of new units. The report does acknowledge the attendant impact development is having on older apartment stock, but infers that this is necessary to generate housing supply and new rental (through strata investment)

While the discussion isn’t likely to end here, it does not appear that there will be any impact on rezoning applications in the near future. The City of Burnaby is effectively keeping things status quo for now.

District of North Vancouver – Rental and Affordable Housing Green Paper (Nov 2, 2015)

Purpose of Report

“This report…provides an overview of the housing situation in the District and identifies the key issues for rental and affordable housing. Through the implementation of the Official Community Plan and other relevant policies, and the administration of the land development application and review process the District has an opportunity to advance key objectives towards protecting existing rental stock and creating more affordable housing.

Emerging developer interest in redeveloping existing rental, and older fractional interest multi-family residential properties in the District has prompted concerns from Council over the potential loss of older, more affordable purpose built rental and low end market ownership units and the potential displacement of lower to moderate income residents.”

Snapshot of Rental Housing in District of North Van

- 9,020 total market rental units

- 4,500 estimated secondary suites

- 850 strata rental units

- $1,209 average rent per month

Key Housing Challenges in the District of North Van

- High housing prices relative to income

- Aging purpose built rental housing stock and lack of renewal

- Almost 90% of 1,269 rental units built before 1980

- Existing rental at risk for redevelopment (over half of stock in town centre areas)

- Displacement of tenants an issue through new market rents

- Apartment vacancy rate is under 1%

- Lack of options for rental for families, students and seniors

- Expiring operating agreements for co-ops and non-profit societies

- Growing homeless population

Potential Tools to Consider

Below is an outline of some of the tools DNV planning staff are examining and considering to address some of the issues above.

- Update Standards of Maintenance Bylaw to improve effectiveness

- Establishment of DNV Housing Corporation to acquire and operate rental

- Amending 1:1 rental replacement to acquire fewer but more affordable units

- Phasing development to replace existing rental

- Create a rent bank

- Priority processing and potential density bonus for rental applications

- More affordable housing incentives in rezoning including CACs to fund

- More affordable ground oriented housing / market value restrictions

CONCLUSION

The District of North Van appears to be taking these issues quite seriously and in fact staff has indicated that they will not consider new applications involving rental housing until these issues are more thoroughly explored.

This may lead to a new rental and affordable housing policy that could potentially impact future rezoning applications. Time will tell which measures actually get implemented. In the short term, the above analysis will almost certainly have the negative effect of slowing rezoning and development applications.

As older rental stock continues to age through Metro Vancouver, we’re likely to see more municipalities exploring ways to address housing affordability, primarily on the rental side.

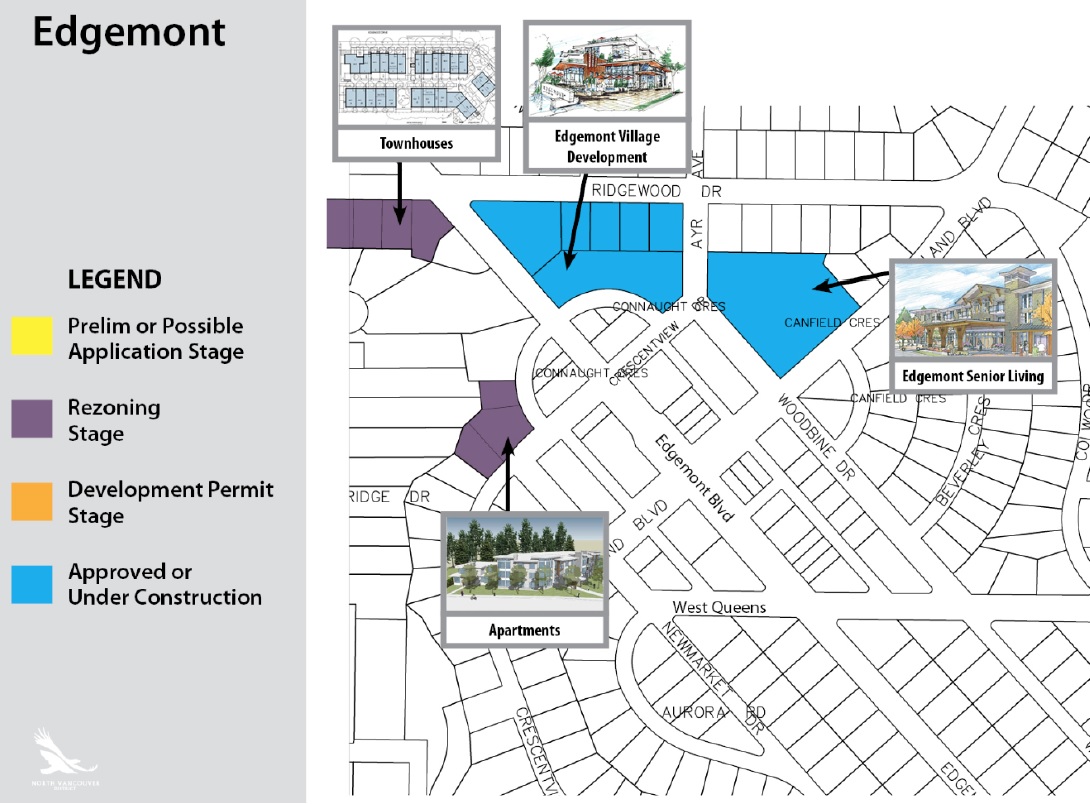

Edgemont Village

Edgemont Village

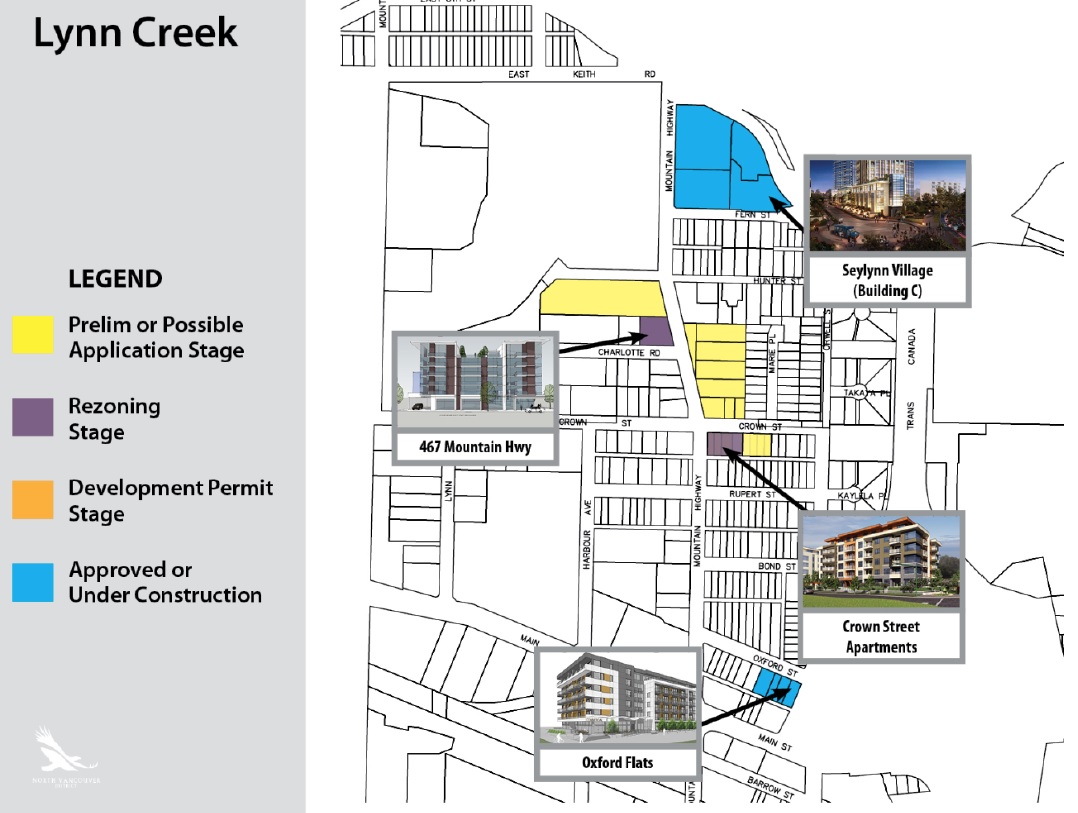

Lynn Creek (formerly Lower Lynn)

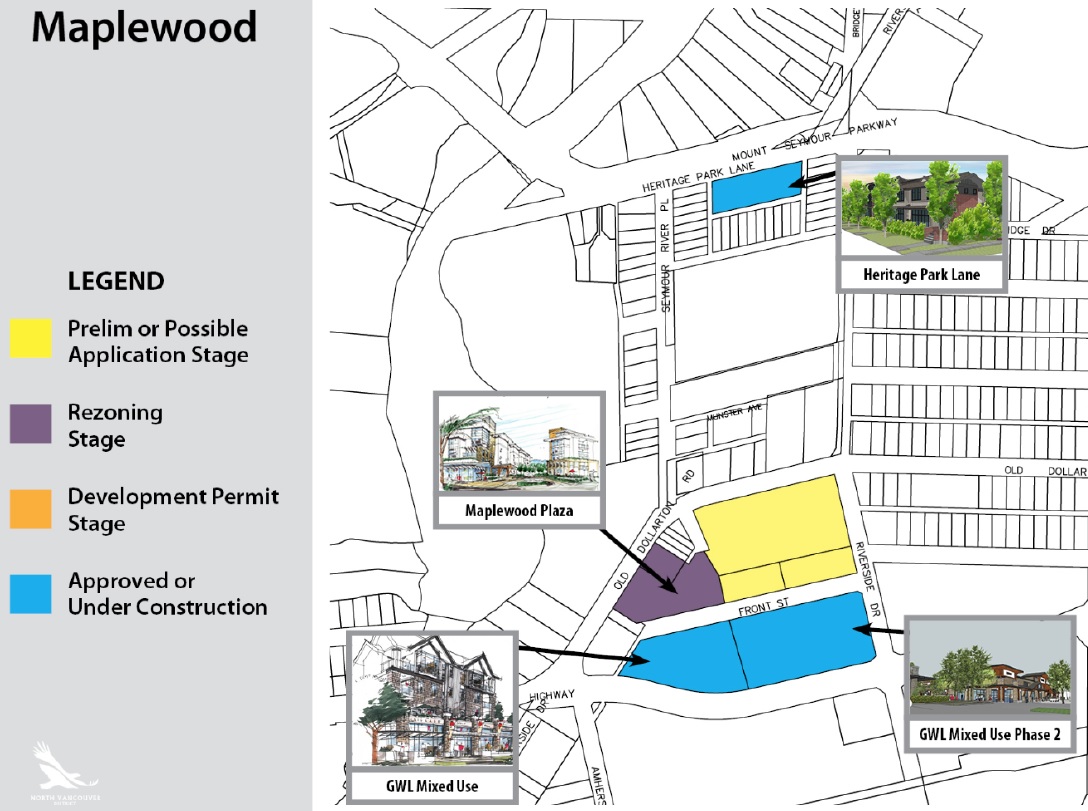

Lynn Creek (formerly Lower Lynn) Maplewood

Maplewood